Clarence Thomas is a real one.

I wish we could clone 8 more of him.

Because this is a true and authentic analysis that actually holds up to Constitutional scrutiny.

Extremely well said:

🚨 BREAKING: SCOTUS Justice Clarence Thomas dropped straight TRUTH BOMBS in his dissent on the tariffs

— Eric Daugherty (@EricLDaugh) February 20, 2026

He nailed it.

"NEITHER the statutory text nor the Constitution provide a basis for ruling against the President." 🔥

"Congress authorized the President to “regulate . . .… pic.twitter.com/nhKtBQ669Y

🚨 BREAKING: SCOTUS Justice Clarence Thomas dropped straight TRUTH BOMBS in his dissent on the tariffs

He nailed it.

“NEITHER the statutory text nor the Constitution provide a basis for ruling against the President.” 🔥

“Congress authorized the President to “regulate . . . importation.” Throughout American history, the authority to “regulate importation” has been understood to include the authority to impose duties on imports.”

“The meaning of that phrase was beyond doubt by the time that Congress enacted this statute, shortly after President Nixon’s highly publicized duties on imports were UPHELD based on identical language.”

“The statute that the President relied on therefore authorized him to impose the duties on imports at issue in these cases.”

“Because the Constitution assigns Congress many powers that do not implicate the nondelegation doctrine, Congress may delegate the exercise of many powers to the President.”

“Congress has done so repeatedly since the founding, WITH THIS COURT’S BLESSING.”

Here is the full text of the Clarence Thomas Dissent:

JUSTICE THOMAS, dissenting.

I join JUSTICE KAVANAUGH’s principal dissent in full. As he explains, the Court’s decision today cannot be justified under the text, history, or precedent of the International Emergency Economic Powers Act (IEEPA).

I write separately to emphasize that IEEPA’s delegation of power to impose duties on imports complies with the nondelegation doctrine. Congress delegated to the President a version of the same power that it has delegated to him in many statutes since the early days of the Republic.

The Nondelegation Doctrine

The Constitution vests “[a]ll legislative Powers” in Congress. Art. I, §1. But “the nondelegation doctrine does not prevent Congress from obtaining the assistance of its co-ordinate Branches.” Mistretta v. United States, 488 U. S. 361, 372 (1989).Rather, it prohibits Congress from delegating its “core legislative power”—the power to make substantive rules that deprive individuals of life, liberty, or property—to another branch without an intelligible principle to guide the exercise of that authority. See Gundy v. United States, 588 U. S. 128, 157–158 (2019) (Gorsuch, J., dissenting).

Tariff Authority and Executive Discretion

Tariff authority is not “core legislative power” in the sense that triggers strict nondelegation scrutiny. From the earliest days of the Republic, Congress has delegated broad authority over tariffs and duties to the Executive in foreign affairs contexts.

Act of May 1, 1810, ch. 39, §4, 2 Stat. 605: Authorizing the President to suspend restrictions on trade with foreign nations under certain conditions.

Act of Jan. 10, 1815, ch. 22, 3 Stat. 195: Authorizing the President to impose retaliatory duties.

These delegations reflect the understanding that the President, as the Nation’s chief diplomat and commander in chief, possesses significant discretion in conducting foreign relations, including economic aspects intertwined with national security and foreign policy.

IEEPA and Historical Practice

IEEPA fits comfortably within this tradition. It authorizes the President, upon declaring a national emergency in response to an “unusual and extraordinary threat” from abroad, to “regulate . . . importation or exportation” of property involving foreign interests. 50 U. S. C. §1702(a)(1)(B). Imposing duties (tariffs) is a traditional means of regulating importation, as historical practice and precedent confirm.

See Fed. Energy Admin. v. Algonquin SNG, Inc., 426 U. S. 548 (1976) (upholding presidential authority to “adjust . . . imports” to include monetary charges); United States v. Yoshida Int’l, Inc., 526 F. 2d 560 (CCPA 1975) (upholding similar authority under TWEA, IEEPA’s predecessor).

Justice Gorsuch’s interpretation of two “early congressional debates” as limiting tariff delegations is thus difficult to reconcile with what early Congresses actually did. Congress repeatedly granted the Executive broad discretion over import duties in response to foreign threats or to advance foreign policy objectives.

Conclusion

The Court’s application of the major questions doctrine here is likewise misplaced in the foreign affairs context, where Congress has long granted the President latitude to respond to unpredictable international crises. IEEPA embodies such a grant—eyes wide open—without the micromanagement that the majority now demands.

For these reasons, and those stated by Justice Kavanaugh, I respectfully dissent.

(Note: Justice Thomas’s opinion is relatively brief and joins Justice Kavanaugh’s longer principal dissent in full. The primary dissenting analysis appears in Kavanaugh’s opinion, which Thomas and Alito joined. Thomas’s separate writing focuses on nondelegation and historical delegations in foreign affairs.)

MORE HERE:

After SCOTUS Ruling, President Trump Has MANY Plan “B” Options — Here’s What He’ll Do

In case you missed it, the Supreme Court finally ruled this morning on President Trump's IEEPA Tariffs, striking them down in a 6-3 ruling.

Details here in case you missed it:

So is that it?

Are Tariffs over?

Trump defeated?

Hardly!

He has many Plan B options and it looks like he will be deploying all of them!

We can start with Justice Kavanaugh who gave the roadmap to President Trump on a silver platter in his dissenting opinion:

And there it is.. Plan B

— MJTruthUltra (@MJTruthUltra) February 20, 2026

🚨 Within Justice Kavanaugh's dissent, He says the Supreme Court got it wrong, but says Trump still has all the Cards:

The IEEPA law does let the President impose tariffs during a national emergency (based on its text, history, and precedents).

The… https://t.co/U7O0dD0TIK pic.twitter.com/hRJLQ7QD0i

Closer look here:

FULL TEXT HERE:

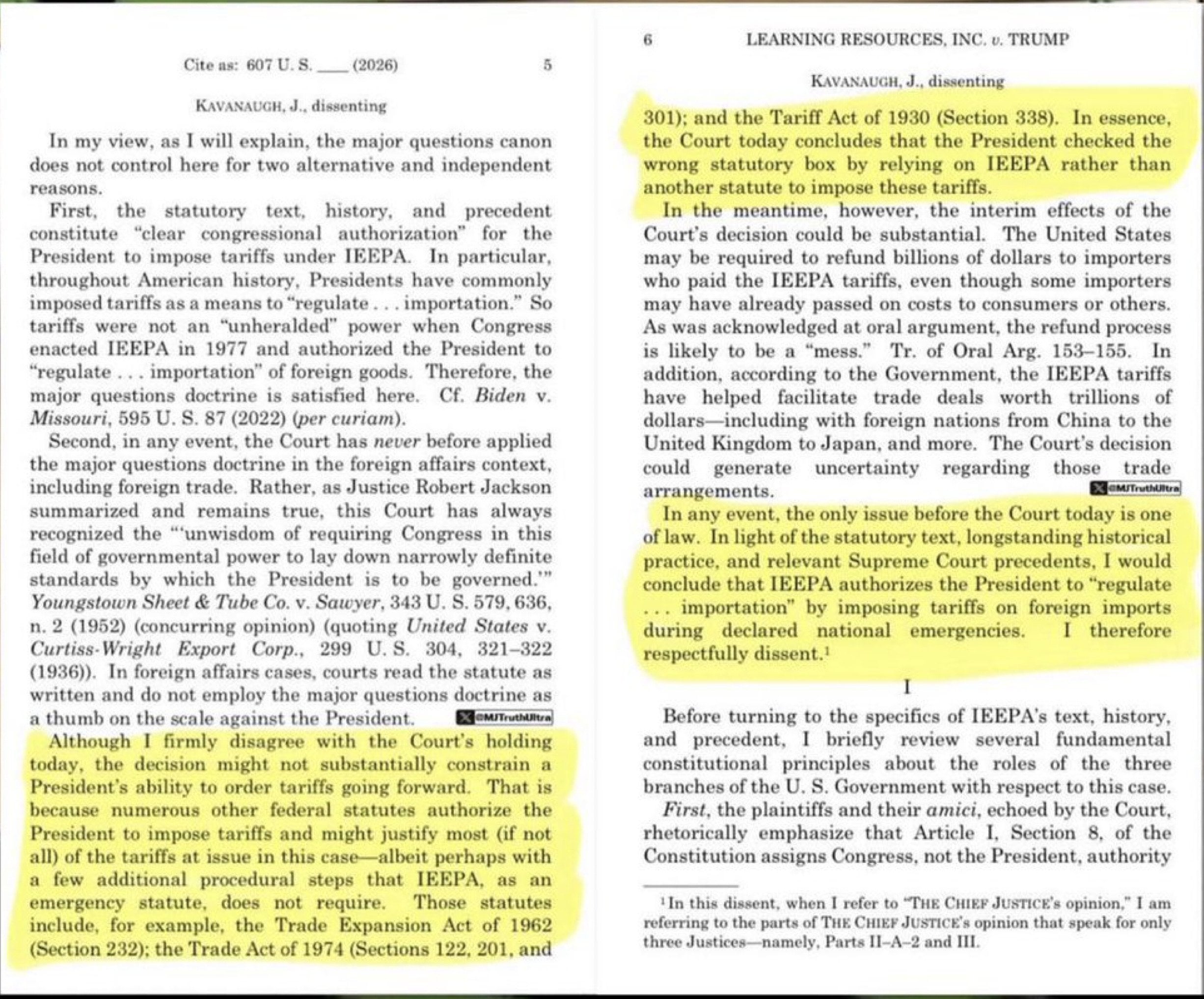

KAVANAUGH, J., dissenting

In my view, as I will explain, the major questions canon does not control here for two alternative and independent reasons.

First, the statutory text, history, and precedent constitute “clear congressional authorization” for the President to impose tariffs under IEEPA. In particular, throughout American history, Presidents have commonly imposed tariffs as a means to “regulate . . . importation.” So tariffs were not an “unheralded” power when Congress enacted IEEPA in 1977 and authorized the President to “regulate . . . importation” of foreign goods. Therefore, the major questions doctrine is satisfied here. Cf. Biden v. Missouri, 595 U. S. 87 (2022) (per curiam).

Second, in any event, the Court has never before applied the major questions doctrine in the foreign affairs context, including foreign trade. Rather, as Justice Robert Jackson summarized and remains true, this Court has always recognized the “unwisdom of requiring Congress in this field of governmental power to lay down narrowly definite standards by which the President is to be governed.” Youngstown Sheet & Tube Co. v. Sawyer, 343 U. S. 579, 636, n. 2 (1952) (concurring opinion) (quoting United States v. Curtiss-Wright Export Corp., 299 U. S. 304, 321–322 (1936)). In foreign affairs cases, courts read the statute as written and do not employ the major questions doctrine as a thumb on the scale against the President.

Although I firmly disagree with the Court’s holding today, the decision might not substantially constrain a President’s ability to order tariffs going forward. That is because numerous other federal statutes authorize the President to impose tariffs and might justify most (if not all) of the tariffs at issue in this case—albeit perhaps with a few additional procedural steps that IEEPA, as an emergency statute, does not require. Those statutes include, for example, the Trade Expansion Act of 1962 (Section 232); the Trade Act of 1974 (Sections 122, 201, and 301); and the Tariff Act of 1930 (Section 338). In essence, the Court today concludes that the President checked the wrong statutory box by relying on IEEPA rather than another statute to impose these tariffs.

In the meantime, however, the interim effects of the Court’s decision could be substantial. The United States may be required to refund billions of dollars to importers who paid the IEEPA tariffs, even though some importers may have already passed on costs to consumers or others. As was acknowledged at oral argument, the refund process is likely to be a “mess.” Tr. of Oral Arg. 153–155. In addition, according to the Government, the IEEPA tariffs have helped facilitate trade deals worth trillions of dollars—including with foreign nations from China to the United Kingdom to Japan, and more. The Court’s decision could generate uncertainty regarding those trade arrangements.

In any event, the only issue before the Court today is one of law. In light of the statutory text, longstanding historical practice, and relevant Supreme Court precedents, I would conclude that IEEPA authorizes the President to “regulate . . . importation” by imposing tariffs on foreign imports during declared national emergencies. I therefore respectfully dissent.

Here is Howard Lutnick from several months ago confirming Trump will implement all of these options if he loses on IEEPA:

Ok… so I did some digging, and yes, it appears President Trump did have a PLAN B if SCOTUS ruled against him.

— MJTruthUltra (@MJTruthUltra) February 20, 2026

The contingency plans include EXPANDED use of Section 232 of the Trade Expansion Act, which allows tariffs on national security grounds and has already been used to… https://t.co/swgz2AGc1R pic.twitter.com/YX2VFtuzR0

Backup video here:

In fact, it's starting already.

President Trump just announced a global 10% Tariff under Section 122:

KABOOM — Your boy called it.💥

— MJTruthUltra (@MJTruthUltra) February 20, 2026

“Effective immediately, all National Security TARIFFS, Section 232 and existing Section 301 TARIFFS, remain in place, and in full force and effect.

Today I will sign an Order to impose a 10% GLOBAL TARIFF, under Section 122, over and above our… https://t.co/5V1Fav8FVl pic.twitter.com/2PSLBI4yI1

Oh man, you have to love this....

President Trump also just declared he was trying to be a "Good Boy" but now the gloves are off and it's "Bad Boy" time!

Looks like he's going full strength ahead and probably even more so than before!

PLAN B — It’s Bad Boy Time 🔥🔥🔥

— MJTruthUltra (@MJTruthUltra) February 20, 2026

President Trump says he was trying to be a “Good Boy”… and let the court do the right thing — but says the GOOD NEWS is that there are methods, practices, statutes, and authorities that are STRONGER than the IEEAP Tariffs, that he still has… https://t.co/5V1Fav8FVl pic.twitter.com/XQHCHSgM7t

Backup here since X/Twitter is crashing bad today:

Fear not my friends....Tariffs are not going anywhere.

The only thing that happened today is that President Trump just sprung into overdrive!

Game on.